Markets By Grant | Digital Behavioral Health

Welcome to Markets by Grant number two.

Remember the fun and light consumer stuff from last week? We sure did have some good times together analyzing the Made-to-Deliver Food market, didn’t we? We smiled, laughed, ate. I told you about my birdwatching hobby (loves animals!) and my relationship history (emotionally available!). I told you that I’m only in New York for a few years, until I meet that special someone and move back to Michigan to raise a family. Near the end of the night, we held hands as I walked you home. You thought, “wow, I can’t believe I finally met him — that nice midwestern guy with kind eyes, an athletic build, and family values. This must be too good to be true!”

You are correct. It’s date number two, and now that I feel I have you on the hook, I’m going to unveil the heavy stuff: the mental health stuff. Hopefully, after all is said and done, you’ll stick with me for Markets by Grant number three.

On a serious note — this is a sensitive topic for many (myself included), and I will do my best to keep the humor delicate and appropriate as I analyze the space. Let’s dive in:

The Market

As is custom, I’ll start with some high-level numbers, but don’t trust them too much:

The Dollars

Digital Behavioral Health (AKA Behavioral Health Software) is modestly high potential, and relatively fast-growing — although this depends on who you ask…

- Market Size in 2020 was estimated at $2.33B, $2.00B, $1.74B, and $1.36B

- CAGR is estimated at 14.8%, 14.6%, 13.7%, and 11%

Result: the powers that be say it’s not that promising of a space, but I’d argue that we don’t really know how to measure it yet.

The People

Why don’t we know how to measure it yet? Because it’s so darn elusive to define its boundaries, capture reliable data, and measure it over time. The behavioral health market is like that pesky ghost in Super Mario. As soon as you look at it, it vanishes. The moment you turn around, it looms.

(Accepting nominations for simile of the year for that throwback video game reference. I’m also in the market for a Gameboy Advance — DM me if selling)

With all that said, I do have some stats for you:

- 20.6% of American adults — 51.5M people — have Any Mental Illness (AMI). These numbers are almost certainly underestimated.

- Among this group, only 44.8% — 29M people — received any treatment.

Of those who remain underserved…

- 41% cited an inability to afford care

- 31% cited an inability to find care.

As proof, 55% of US counties do not have a single practicing psychiatrist. And let’s not forget about sociocultural stigma as a barrier to seeking care.

So What?

Here’s what’s between the lines of all those stats:

- The US has among the world’s highest availability and utilization of mental health services, and yet the unmet need remains massive. As large as this opportunity is, the unmet needs (and underreporting of needs) in foreign markets is exponentially higher.

- COVID brought mental health needs to the forefront, and can be seen as a market tailwind. It has also helped normalize the use of telemedicine and digital solutions (which are also often favorable in terms of accessibility, convenience, and cost)

- Meanwhile, market growth (in the US) is not driven by price, new capabilities, or notable population growth, but instead by saturation and penetration.

The Bottom Line

And here’s my POV on the market overall:

The market potential for behavioral health, especially digital behavioral health, is undervalued.

Technology-enabled solutions for patients can reduce cost and increase access to accelerate market penetration.

Technology-enabled solutions for providers can benefit from the increasing scale of the market by streamlining workflows/costs and differentiating services.

Now, you’re probably thinking, “Grant, why did you just spend 422 words telling me things I already read years ago in an edition of Reader’s Digest I found in between my grandmother’s couch cushions?”

Here are my responses to that (completely uncalled for) attack on my writing:

- I don’t include headers in my word counts, so it was actually only 411 words — ie: fairly concise.

- No way your grandmother still reads that Reader’s Digest smut. She should read Markets by Grant.

- Why were you reading Reader’s Digest when you should have been spending quality time with your grandmother?

- I was just introducing the space — we’ll get into the more in-depth analysis shortly.

The More In-Depth Analysis

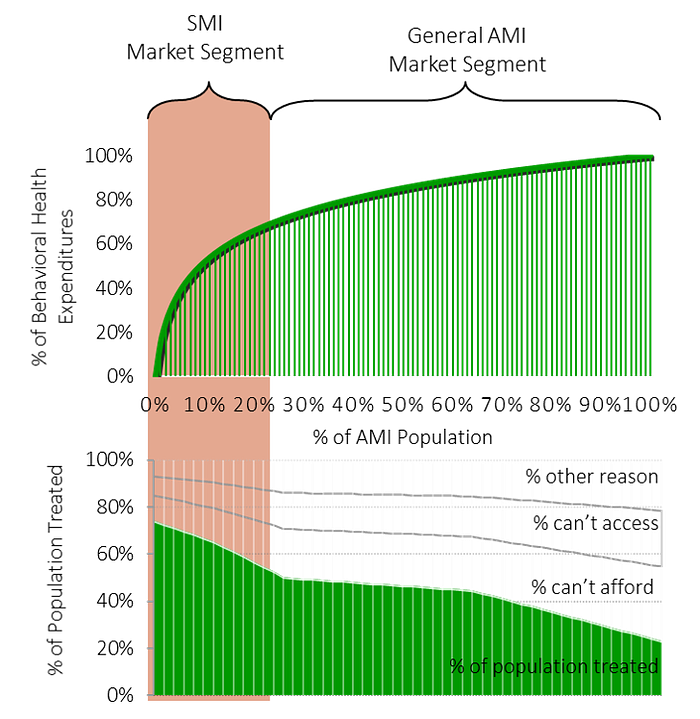

Taking the US (in 2019) as an example:

- 55.2% of the population with AMI (Any Mental Illness) is underserved.

- The top 25% of this group (13.1M people) has SMI (Serious Mental Illness).

- Owing to the more debilitating nature of their illness, more of these individuals (65%) seek treatment, and they account for a disproportionate amount of overall market expenditures.

To get a sense for the user market, take a few minutes to let this chart sink in:

This suggests a tradeoff for startups targeting their market entry:

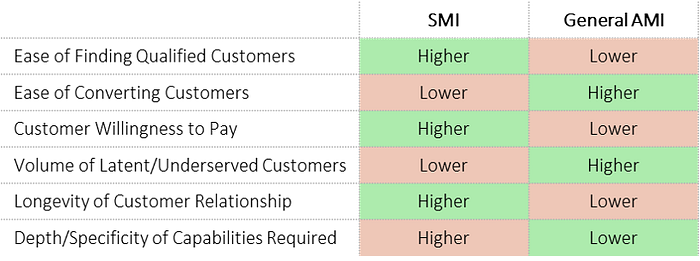

- The SMI segment of the AMI market is, in economic terms, more saturated with services, but also much more lucrative on a per-customer basis.

- In other words, the burden of differentiation to convert customers may be greater, but the lifetime value of a customer may be higher.

- Conversely, while more latent supply exists in the ‘long tail’ of the underserved masses, significant social/cultural barriers and stigma exist — making the likelihood of swift market penetration unlikely. The average delay between onset of mental illness symptoms and treatment is 11 years.

More graphically put…

A plethora of substitutes adds to the challenge of AMI market penetration:

- Substitutes are plentiful, and are positioned to treat the symptoms individuals may otherwise seek to resolve with behavioral health interventions. These include exercise, entertainment, drugs & alcohol, OTC medicines/supplements, social activity, etc.

- These ‘avoidant’ fixes for dealing with underlying mental illness have more noticeable immediate effects on symptoms than therapies and prescription medicines, and may come at less social/financial cost. In the long run, however, they may prove to exacerbate symptoms. Their use is therefore self-reinforcing, and challenging to overcome.

Now that we have a more nuanced view of the market, let’s dive into the existing landscape, which I’ve broken into three segments:

The Landscape

- Most of the startups in this space have started from the ‘ground floor’ — capitalizing on early adopters of telemedicine and the task-oriented, rules-based nature of CBT (cognitive behavioral therapy) to digitize existing offerings, in the broadest, most general sense — for AMI audiences.

- To be fair, these “breadth over depth” services are often more palatable to sell to insurance companies, employers, and health systems, who are favorable “big fish” for winning recurring revenue streams.

- As a result, white space exists at the SMI market segment, not just for “Serious” Mental Illness, but also for “Specific” Mental Illness.

The Opportunities

With all this in mind, I want to revisit my “bottom line” above — with patient-facing and provider-facing strategies which capitalize on market opportunity by increasing access, decreasing cost, streamlining processes, and differentiating services.

Strategy 1: ‘Verticalized’ Digital Behavioral Health

This strategy involves selling “depth over breadth” directly to patients — more targeted, specific offerings for people suffering through what they view as specific issues. Examples are solutions focused on adolescent depression, substance abuse, relationship counseling, PTSD, etc. Here’s what I mean, more specifically:

- Mental health professionals would argue that regardless of the subject matter, mental health disorders exhibit very similar underlying thought patterns, and can therefore be treated with the same approach. With this in mind, generalist ‘breadth over depth’ platforms do address patient needs. The problem here is not in the methodology, but the funnel.

- At the top of the funnel are individuals who feel their struggle is just that, individual. These individuals are less likely to diagnose themselves as having a broad, general mental health illness (I’m depressed, and my symptoms are just the same as anyone else with depression) — and are more likely to search for help in a specific area they feel is directly applicable to them (ie: I’m struggling with trauma). This is especially true for individuals who are new to behavioral health treatment.

- Once patients are converted, they’ll be stickier and more engaged to a community and process they feel is specifically for them, and they’ll be less likely to churn. By definition, this verticalization creates differentiation, and individuals with a specific struggle will be unlikely to instead choose the generalist solution.

- Finally, platforms also have a higher value proposition for providers who are specialized — allowing them to practice their preferred specialization and contribute to a community of knowledge in their area of expertise.

Here are a few startups I’m following which employ this strategy:

Strategy 2: AI Provider Augmentation.

On the mental health provider side, white space exists in provider tools — HIPAA-compliant solutions which capture patient data to aid provider decision-making and streamline administrative effort. Promising solutions use AI to make connections, prioritize activities, and surface recommendations. Here’s why:

- Aside from digital therapeutics, innovation in care delivery and patient data analysis is nascent. Few players are using AI to better understand mental illness, and fewer still are equipping providers with the power of these insights.

- Compared to telehealth platforms/online clinics and digital therapeutics, innovation in tools for providers has been lackluster — despite the fact that they are the most critical intermediary in the behavioral health delivery process. Providers are critical buyers, with high willingness to pay, who have been underserved in the market.

- Rather than being on the receiving end of a telehealth platform war, an opportunity exists to empower providers with digital tools to augment their practices and capabilities — with the opportunity of improving revenues due to higher patient volume served, reducing administrative costs (and costs of relapse), and, of course, improving patient care.

Here is a startup I’m following which employs this strategy:

Wow, that was a long one. If you stayed with me for the whole thing, bless you. If you did not stay with me but instead skipped to the bottom in hopes of a TLDR, I will give you no such satisfaction. Stand up, stretch, sit back down, and ingest the rest of this top-notch content. After you do so, don’t forget to roast me in the comments section.

Until Next Week,

— G

References:

- https://www.fiercehealthcare.com/tech/funding-for-digital-behavioral-health-startups-surged-amid-covid-19-pandemic

- https://www.globenewswire.com/news-release/2021/02/23/2180320/0/en/Rising-at-14-6-CAGR-Mental-Health-Software-Market-Size-to-Register-USD-3-957-Million-By-2025-Covering-COVID-19-Global-Analysis-Facts-Factors.html

- https://www.grandviewresearch.com/industry-analysis/behavioral-mental-health-care-software-market

- https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2013.0769

- https://www.marketdataforecast.com/market-reports/mental-health-software-market

- https://www.medicalstartups.org/top/mental/

- https://www.nami.org/mhstats

- https://news.crunchbase.com/news/access-to-mental-health-startups-tackle-sectors-complexities-as-investors-go-all-in/

- https://www.nimh.nih.gov/health/statistics/mental-illness.shtml

- https://www.nytimes.com/2020/12/07/business/mental-health-start-ups-teletherapy.html

- https://pitchbook.com/news/articles/mental-health-startups-venture-capital-outpace-2019

- https://techcrunch.com/2020/11/23/mental-health-startups-are-raising-spirits-and-venture-capital/